Tis’ the season for food truck and food trailer owners to get a much-deserved rest and break from the daily grind of the busy summer season. Unlike restaurants, chefs and caterers, who are well into the busy holiday season.

Unfortunately, this time of year has historically been when thefts spike. Thieves have to buy Christmas presents too, right? Here are some tips to help avoid becoming a victim of theft in your food business.

Lighting

When you are not able to secure property in a closed off or secure area, lighting is a great tool to deter would-be thieves! Lights help increase the chance someone will see a theft. That reason alone is enough for thieves to move on to their next target.

Parking near overhead lights works great, but if that is not an option, this Solar LED light with Motion Sensor can easily be installed and a great way to illuminate the area around your property.

Locking up

It’s good business practice to let customers know when you are open or closed, but that makes it easy for thieves to know when you are not around! Locking up is a good first step, but a determined thief that knows he has time when you are away might have tools to bypass basic locks.

A client of Insure My Food, Matt with Las Abuelas, recommends using a Shackle-Less Padlock like the ones found here on Amazon. By not having an exposed shackle it makes it impossible for bolt cutters to be used.

For food trailers, hitch locks are a must. While they might not be bulletproof, they are important! Yes, a lock can be forcefully removed or the thief could use a flatbed tow truck to bypass the hitch, but for under $30 dollars it’s well worth the investment and enough to give a thief a reason to move on.

For food trucks, a steering wheel lock is a great idea. Most of the step van trucks used to build food trucks date back 20-30 years ago. They lack the update ignition protections that modern vehicles have. This makes it easy for thieves to hotwire and drive off with your truck.

Make some noise

Noise is a great way to draw attention to your property so others around look and know something is not right. Sounds can be very annoying, as Jim Carey taught in Dumb and Dumber.

Alarms that are loud and also report to a monitoring service are great but can require a constant internet or phone connection and that can be difficult for a mobile food vendor. They require a monthly service cost increasing your business costs. If the connection or the cost is prohibitive, having an audible alarm is inexpensive (GE makes a wireless door alarm for under $12) and an effective solution.

Cameras

Visible cameras protecting your business let crooks know they’re being watched and are very helpful in deterring theft. Cameras help you review suspicious activity so that you can be proactive prior to a theft occurring.

Trackers are a great way to keep tabs on your property, but they do require a monthly subscription for services. GPS trackers are also not a replacement for other theft prevention practices because they only help when your entire truck or trailer is moved offsite.

Take cash to the bank

Having a lot of cash attracts attention not only from outside threats but from employee theft as well. Making frequent trips to deposit cash and never leaving cash overnight is a great step to limit theft of your hard earned money. Hope of Emoji’s Grilled Cheese took it a step further and now only accepts credit and debit, eliminating the risk altogether. She states that she has had very little pushback from customers.

With a little effort and investment, taking the some of all of the above steps will go a long way in reducing the risk of becoming a victim of a grinch during this season. Check out our loss prevention blog post for more tips on How To Protection Your Food Truck’s Bottom Line.

Want an insurance quote? Click here or give us a call at (800) 985-7859.

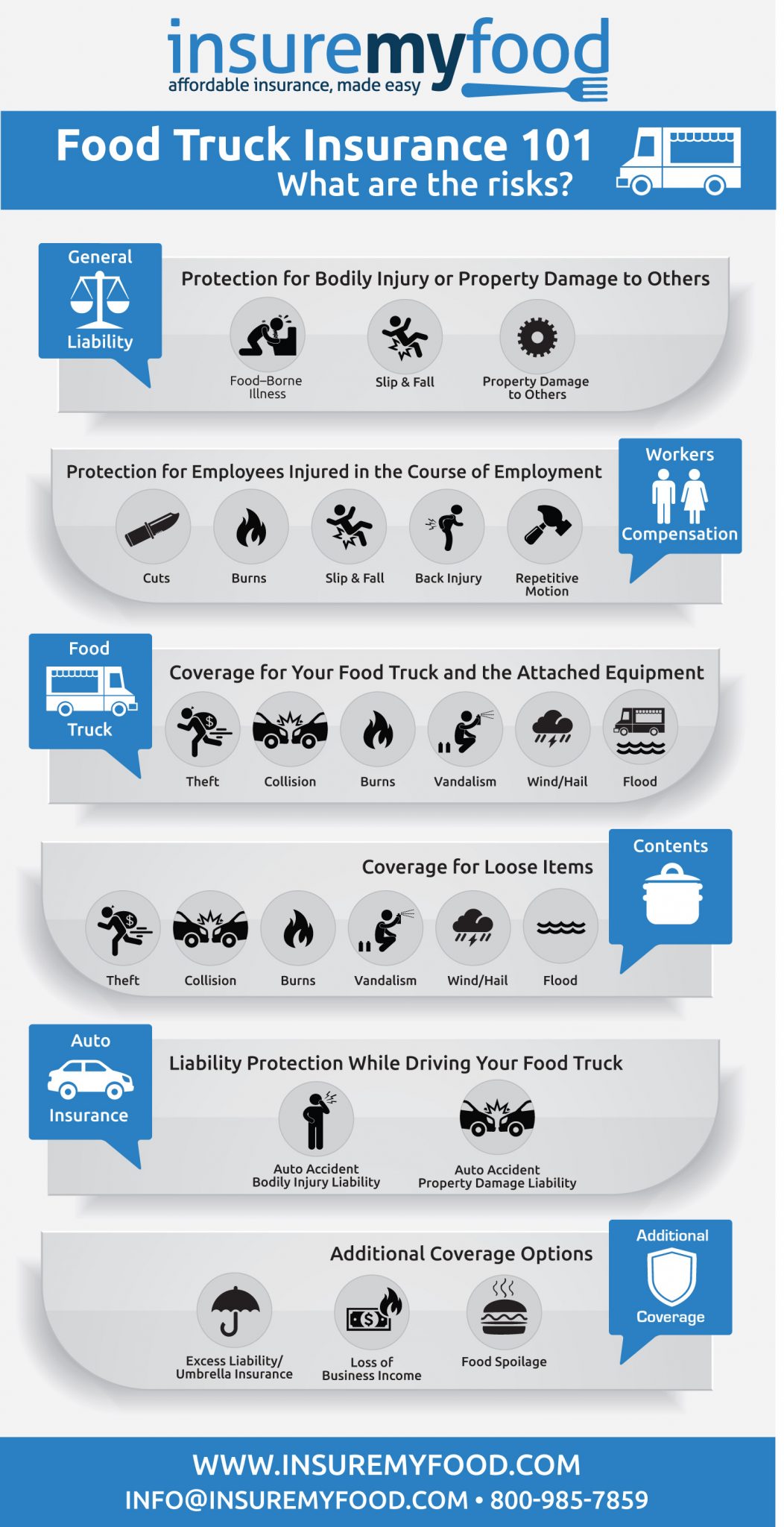

Confused by the complexities of food truck insurance coverage and not sure what exactly you need? We get it. It can be confusing, so we’re going to break down the different types of coverage for you using understandable language (and not insurance-gibberish).

First, take a look at the visual cheat sheet we’ve created. Below that, we’ll get into the specifics of each type of insurance to give you a well-rounded understanding of your specific needs and insurance options.

Save this graphic and keep it handy so you always know what you have covered and what you don’t. Now, let’s go a little deeper into these food truck insurance coverage types.

General Liability Insurance

Whether you’re after bare bones protection or a full suit of armor around your business, this coverage type is a must.

General liability acts as protection against lawsuits brought against you. It covers your products (food and drinks), your premise (slip and fall), personal injury (including libel and slander), and property damage to others.

Keep in mind that this type of insurance covers damages to others, but it does not cover you, your employees being injured, or damage to your own vehicle. Nor does this coverage effective for accidents that occur while you’re driving.

A few specific instances where general liability covers damages:

A customer gets sick from your food

A customer slips and falls on a mat you placed outside

Another business accuses you of libel or advertising injury

Your patio cover falls and breaks another truck’s window

All the legal fees associated with the incident (even frivolous claims where you are not at fault)

The common coverage limit is $1,000,000 per occurrence and $2,000,000 total per year.

Most landlords, vendors, and commissary kitchens require general liability, so you should plan on including it in your policy.

Property insurance coverage for your truck and the attached equipment

Don’t let the countless hours you invested into your food truck go to waste with a single driving mistake or a severe stroke of the weather. Food truck coverage protects your truck and all its attached equipment in the event of a collision, vandalization, theft, flood, fire, and a few other types of losses.

Remember that “attached equipment” specifically refers to items that are attached via bolt, plumbing, or gas line. Plates, pans, rolling carts, food, and anything else that’s not securely bolted down is not covered by this coverage. For those items make sure you get contents coverage (listed below) as well.

Coverage for items NOT attached to your Food Truck

Contents coverage is for all the things that are not bolted down or attached via plumbing or gas line, but are still a part of your food truck business. Your cooking utensils, your chairs, and even your POS system fall into this category.

Auto Liability

Your greatest liability risk as a food truck owner is not the food you serve, but the truck you drive. Food-related claims are uncommon, but driving mistakes on the road happen all the time.

Auto liability insurance covers injury or property damage to others while you are driving, and only when you are driving. Once you are parked and open for business, your general liability coverage takes over.

Workers Comp

Worker’s compensation insurance (commonly known as “worker’s comp”) covers you when your employees are injured while on the job. With this type of coverage, injured employees will have access to wage replacement pay and medical benefits.

Most states require you to carry worker’s comp insurance by law, but a few leave it optional. If you’re not sure what the law says in your state, The National Federation of Independent Business offers a state by state list of workers comp requirements.

Additional Coverages

There are a variety of coverage “add-ons” available to suit your specific needs. Let’s take a look at a few of the more common add-ons.

Umbrella insurance – Worried a claim cost may exceed the basic limits of your coverage? This add-on extends the financial benefit to cover large claims and is often required by large contracts.

Food spoilage insurance – Serve a certain type of food that tends to spoil quickly? This insurance will keep it from eating into your bottom line.

Loss of business income insurance – If you suffer a collision and have to get your truck repaired or replaced, the lost income over days or weeks can end up being thousands of dollars. This coverage type compensates you for that lost income and is, in our minds, one of the best additional coverages.

There’s a whole slew of add-ons, so if you have any uncommon truck features or business practices, let us know and we’ll find the right coverage.

About Insure My Food

Insure My Food provides insurance coverage for an array of mobile food vendors such as food trucks, food trailers, concession trailers, pop, vendors, concessionaires, snow cone stands, and more. Our goal is to help you protect your business with insurance that fits your specific needs so that you can focus on the aspects of your business that matter most.

We have over a decade of insurance experience and a deep understanding of the often complex (and ever-changing) mobile food industry. We also partner with several different insurance carriers to make sure your food truck process is affordable and easy.

Want an insurance quote? Click here or give us a call at (800) 985-7859.

If you are not convinced you need proper insurance for your mobile food business, let me share 7 reasons why you should think again!

1) It’s the law. States require all vehicles on the road to carry insurance, even if you do not plan on moving around much, you are required to have auto insurance on a food truck.

2) Opens up opportunities. Without a general liability policy on your food truck, events, landlords, and commissary kitchens won’t work with you. <link to AI blog>

3) Sound risk management and peace of mind. If you invest thousands into your food truck and countless hours building your business you don’t want to see it end in a split second from an accident or theft. Check out our blog on Loss Prevention for a handy checklist to keep your business protected.

4) It’s socially responsible. The last thing you want to do is injure someone or damage their property with no way to help. Insurance provides a means to compensate others for accidents.

5) Protects your employees. Employees are often like family (or ARE family), and Workers Comp insurance compensates them and pays medical bills if they are injured doing their job. Still not convinced? We wrote a whole post on the disadvantages of not having Workers Comp Insurance.

6) Legal fees paid for. Insurance companies pay attorney’s fees for insurance claims on your behalf. Even for frivolous claims.

7) Protection for your assets. Accidents happen. Without insurance, your assets and your business are on the line.

Insure My Food offers affordable insurance made easy for food trailers, food trucks, and mobile food vendors. We offer a one-page quick quote form, or check out our other blogs for more tips!

Not sure what your food truck is worth? There are quite a few things to consider – and the trucks themselves can be just as unique as the chefs who operate them.

We get it. You don’t have much time to figure it all out – but you need to. Knowing a food truck’s value is essential in these circumstances:

Buying a food truck

Selling a food truck

Insuring a food truck

With a bad estimate, you risk losing lots of money on the sale or underinsured insurance claim. With an accurate estimate, you can be financially confident and satisfied with your business journey from start to finish.

Lucky for you, we’re going to make this as easy as it can be!

Let’s start with the basic formula for determining food truck value.

Food Truck Value = Cost Of The Truck + Cost Of The Attached Equipment + Labor Cost To Install Equipment

This applies universally, whether your truck is a brand new restaurant on wheels, a second-hand truck, or even a converted school bus.

Next, let’s breakdown each variable in the formula:

Valuing The Truck Itself:

Start by evaluating what your food truck is worth without all the gear and equipment. In insurance language, this is the “Actual Cash Value” or “Current Value” of the truck.

Tip: Items not attached to the truck but kept inside the truck are not part of the truck value. Instead, they’re classified by insurance companies as “Business Personal Property” or “Equipment Not Attached”.

New Truck:

If you have a new truck or are looking to buy a brand new one, you’ve got it easy. There’s no depreciation to factor in, so the value of the truck is simply the amount you paid (the sale price).

Used Truck:

Most people dread the process of finding the value of a used truck, but it’s actually quite simple in most cases. Here’s what you need to do:

Search for the same truck online. You should be able to find the same model and year (and rough mileage) on eBay or Craigslist, which will give you a strong estimate of your used truck’s value.

Add in your improvements/investments. Update the engine, replace the transmission, or make other improvements? Add those costs to the value of the truck.

Don’t add the truck’s cooking equipment in just yet. We’ll get to that next.

Valuing Attached Equipment:

Now we’ll assess all the equipment that’s attached to your truck. And when we say attached, we mean permanently built-in by bolts, plumbing, or a gas line.

Tip: Flip the truck upside down. Anything that stays put can be categorized as “Attached Equipment”.

Tip: Don’t actually flip over your truck.

New Equipment:

This part is easy. Simply add up the cost of the equipment, as well as the cost of the labor to install the equipment. Even if you did the work yourself, you can still add an estimated installation cost to your equipment’s value.

Used Equipment:

Valuing any used equipment is a bit more tedious, but not difficult. Here’s how we suggest doing it.

Take inventory of all your equipment. A sheet of paper or excel document will do fine.

Search for used items online. Search for the same items on buy-used sites like eBay or Craigslist to make a value estimate.

When it comes down to it, you’re making estimates. So if you can’t find the used price for an item, don’t worry – just make an educated guess using this next mini-guide.

How to estimate depreciated value:

There’s really only one “rule” you need to keep in mind when estimating depreciated value: generally, kitchen equipment depreciates over a 20-year life cycle. You then need to discover the age of the item, as well as the cost of the item brand new.

From here, it’s actually a simple process.

Discover the percentage of life lived. For example, equipment that’s 5 years old has lived 25% of its 20-year life cycle.

Subtract that percentage from the brand new price. If the item was $1,000 brand new, subtracting 25% leaves you with a $750 value.

Add in labor costs. If it costs $50 to install that item (whether you did it yourself or hired someone to), the equipment value then becomes $800.

Don’t forget about aftermarket additions. Did you add any graphics, paintings, wraps, or other permanently attached items? Add those as well.

If you need help with this process, your Food Truck’s original builders can also be a source for valuing the attached equipment. Check out our list of Food Truck Builders Resource Page.

Tip: Create a list of equipment and value during this process to reference in the event of a claim.

You should now be able to plug in all the needed numbers for this formula to find the value of your food truck.

Food Truck Value = Cost Of The Truck + Cost Of The Attached Equipment + Labor Cost To Install Equipment

Non-Attached Equipment:

Equipment in your food truck that’s not permanently attached to the truck is its own separate coverage and limit of insurance. Here are a few examples of these items:

Blenders

Table Warmers

POS System

Pots / Pans

Non-Bolted Refrigerators

Tip: Have any strapped down tools and items? Those are also considered “Not Attached”. It must be bolted down or attached by plumbing or gas line to be considered “Attached”.

Valuing this equipment takes the same process as valuing attached equipment. Brand new gear is just the new price. Used gear’s depreciated value can be calculated using the 20-year life cycle. However, there’s no labor to calculate with these items.

—

See? It’s not such a bad process after all. However, if you’re still scratching your head, there’s no need to worry. Give us a call – we’re happy to help!

Insure My Food offers affordable insurance, made easy! We cover insurance for food trailers, food trucks, and mobile food vendors. We offer a one-page quick quote form. In addition, we created helpful blogs and resources just for you. Joel brings over a decade of insurance experience in helping you determine your proper food trailer insurance coverage.

So you’ve decided that you are going to open up a food trailer or food truck in San Antonio. Congratulations! We have created a basic outline to help you with the necessary steps needed to open up your business. Although the outline is intended specifically for mobile food vendors in San Antonio, TX, the process and regulations are often similar in different cities and states. You can use this outline for starting either a food truck or food trailer.

Step 1: Filing a Limited Liability Company For Your Food Trailer

It is very common for foodservice businesses to form an LLC. You can find out more info here.

Step 2: Texas Sales and Use Tax Permit

Before you can receive your Mobile Food Vendor Permit you will need to have a Texas Sales and Use Tax Permit. You can find out more information here.

Step 3: Do Your Research and Join the SAFTA

The San Antonio Food Truck Association is a coalition of trucks working together for the betterment of the mobile food community. Look into joining and also look for owners who may be willing to mentor you or share their experience working within city limits.

Also, the City of San Antonio has a helpful page on gathering the items you’ll need for your mobile vending business by category. Current regulations for the city are also listed here.

Step 4: Buying a Food Trailer or Food Truck

Although you may be able to find good deals on Craigslist for used food trailers or food trucks, there are also many great food trailers and food truck builders in Texas! One benefit of buying a newly manufactured food trailer is that the builders are usually knowledgeable about requirements to pass a City of San Antonio Health and Fire Inspection. You will also have peace of mind knowing that all of your equipment is new and not damaged or aging.

Step 5: Buying Insurance for Your Food Trailer or Food Truck

We recommend purchasing $1,000,000 worth of liability insurance and property coverage on your food trailer or food truck as soon as you purchase so that you are immediately protected from accidents or theft. We have two helpful blogs that dive deeper into your coverage options:

TIP: Many landlords require you to have $1,000,000 worth of general liability insurance before they will let you sell food on their property.

Step 6: Registering Your Food Trailer or Food Truck with the DMV

Before you can apply for a Mobile Food Vendor Permit, you will need to register your trailer with the Texas Department of Motor Vehicles here.

Step 7: Get Your Food Managers Certification For Your Food Truck

In order to pass your health inspection, you will need your Food Managers Certification displayed inside of your food trailer. You can find out more information and testing options here.

TIP: We suggest paying a bit extra to have your Food Managers Certification stay valid for 5 years because the class takes a full workday day to complete.

Step 8: Get Your Background Check

Request your background check at SAPD Records Unit at 214 W. Nueva (8 am – 4 pm.) The fees for local, state and national background checks are $59.25, only cash or money orders are accepted as payment. You will receive a response BY MAIL after the local and DPS background checks are completed (4 – 6 weeks.) This statement will remain valid for 90 days from the issue date.

Step 9: Set Your Appointment for Inspection

This is the packet that you will need to submit to the Health Department before they will inspect your food trailer or food truck and issue you a Mobile Food Vendor Permit. Mobile Vending inspections are done on Tuesdays and Thursdays by appointment. Appointments may be made by calling 210-207-8853. Inspections will be conducted at a site designated by the vendor (must be in City of San Antonio limits and not residential property).

In order to pass inspection, you must find a Central Prep Facility to use. Many food trailers and food trucks use their CPF strictly to dump grey water, get fresh water, and dump grease.

There are currently seven approved commissaries in San Antonio that can issue Notarized Commissary Letters that will be honored by San Antonio Metro Health. Those facilities are listed:

Alamo Kitchens – 11825 West Ave, Ste 102, San Antonio, Texas 78216

The Co-Op SA- 11911 Crosswinds Way #305 San Antonio, TX 78233

Congratulations on passing your inspection and getting your clearances! You are now ready to roll. Be sure to check out the City of San Antonio’s website for all regulations that need to be followed.

TIP: Mobile vendors in residential areas can only operate from 7 am to one half-hour after sunset. In the months of June, July, and August, those units may extend their hours of operation to 10 pm.

Insure My Food was designed by an insurance agency that gets food trailers and food trucks

We understand the challenges and needs of your business and are committed to supporting the mobile food community.

Not only do we offer food trailer and food truck insurance in almost every state, we insure many types of mobile food vendors including concession trailers, food carts, pop-up vendors, street vendors, food stands, and catering trailers.

Contact Us for a free, no-obligation quote or if you have any further questions. From our small business to yours, we’re here to help you succeed!

No doubt, you have poured countless hours, and what seems like an endless amount of money to create your food trailer, concession trailer, or food truck business. It makes sense to protect those investments with a good loss prevention plan to prevent all those efforts from being ruined in an instant!

Loss prevention:

An often overlooked first step by many mobile food vendors…how do you prevent a loss from ever occurring?

This is a smart first step for savvy business owners. Insurance policies will have deductibles to encourage loss prevention and being shut down due to a loss is a huge burden worth avoiding.

1) Inventory your items. This can help recover stolen items and provide a guide to insuring for the proper amount. In the event a claim does occur, your preparedness will speed up the process.

2) Good lighting at night and visibility go a long way in protecting from vandalism and theft. Think solar lights, motion detecting lights, etc. There are also a plethora of inexpensive cameras/monitoring devices that are well worth the investment.

3) Take extra precaution in securing high theft items such as generators, cash, and computers. Keep them out of sight and secured when not operating.

Even the most cautious food trailer, food concession trailer, and food truck owners can suffer a loss. Unless you’re prepared to replace your truck, trailer, or equipment out of your own pocket, insurance is a smart way to transfer that risk to an insurance company.

1) Determining the proper value for your truck and trailer is step one. The amount you should insure your truck or trailer for is the actual cash value. In other words at the current value, not the value it would cost to buy a brand new truck or trailer. This total should include any equipment attached by bolt, pluming, or gas line. To read more check out our other blog post, What is the value of your food truck or trailer?

2) Your contents not attached to your food truck or food trailer are NOT covered by the coverage on your truck or trailer. These items can be listed under contents separately. If there are any items over 2500 in value, they will need to be reported to the insurance company.

3) Since insurance companies typically insure property at a specific location this can cause gaps in coverage for mobile food vendors. You want coverage for property that regardless if you are heading to an event or at your main location. The term used for property that moves locations is called inland marine insurance; it’s a must for a mobile food vendor.

4) If you upgrade or buy more equipment always notify your insurance carrier right away.

Common Mistakes:

1) Thinking your auto or home policy extends to your trailer for property coverage.

2) Having a policy that only covers you at the address listed on your policy.

3) Assuming contents not attached are covered with your coverage on the truck or trailer.

Insure My Food offers affordable insurance, made easy! We cover insurance for food trailers, food trucks, and mobile food vendors. We offer a one-page quick quote form. In addition, we created helpful blogs and resources just for you. Joel brings over a decade of insurance experience in helping you determine your proper food trailer insurance coverage.

Joel Paprocki, CIC, CRM, CPCU is founder of Insure My Food. Joel has over 20 years of experience in the insurance industry. He is passionate about helping food entrepreneurs navigate insurance and risk management with confidence. He holds all three top industry designations: Certified Insurance Counselor, Certified Risk Manager, and Chartered Property and Casualty Underwriter. He has served over 5,000 clients in the food industry, including restaurants, food truck, cateriers, If you are looking for a reliable, experienced, and specialized insurance partner, please contact us.

Joel Paprocki, CIC, CRM, CPCU is founder of Insure My Food. Joel has over 20 years of experience in the insurance industry. He is passionate about helping food entrepreneurs navigate insurance and risk management with confidence. He holds all three top industry designations: Certified Insurance Counselor, Certified Risk Manager, and Chartered Property and Casualty Underwriter. He has served over 5,000 clients in the food industry, including restaurants, food truck, cateriers, If you are looking for a reliable, experienced, and specialized insurance partner, please contact us.

Joel Paprocki, CIC, CRM, CPCU is founder of Insure My Food. Joel has over 20 years of experience in the insurance industry. He is passionate about helping food entrepreneurs navigate insurance and risk management with confidence. He holds all three top industry designations: Certified Insurance Counselor, Certified Risk Manager, and Chartered Property and Casualty Underwriter. He has served over 5,000 clients in the food industry, including restaurants, food truck, cateriers, If you are looking for a reliable, experienced, and specialized insurance partner, please contact us.