Insurance Overview – Commissary Kitchens / Shared Kitchens

What are Commissary Kitchens / Shared Kitchens

Shared kitchens, also known as Commissary kitchens, have gained popularity in the last 10-15 years, alongside the explosion of food trucks and small food entrepreneurs across the county. Commissary kitchens offer commercial kitchen facilities for small food entrepreneurs such as consumer packaged goods, caterers, chefs, food trucks, or even ghost kitchens. Commissary kitchens provide food entrepreneurs affordability and scalability as they grow their businesses by providing fully equipped and health department-approved shared kitchen facilities.

Risk Management Overview

It is a common misconception that buying insurance is the first and often the only step in risk management. Insurance is just a tool to transfer risk and is only for pure risk (chance of loss or no loss). All businesses also face speculative risks, which are risks with a chance for gain or no gain. For example, buying equipment or starting a new marketing program with hopes for a return on the investment.

For this article, we will focus only on the pure risk that insurance can address, but as a business owner, you should be looking at all risks to the business’s survival and success.

As you address your risk it helps to think about your total cost of risk. The total cost of risk is defined by the cost of insurance, the cost of uncovered claims (retained risk), deductibles, and administrative costs of managing risk. It’s common for small businesses to only look at insurance costs, but having a broader view can help provide a clearer picture to make educated risk decisions.

Identify Risk

The first and most important step is to identify the risks your commercial kitchen faces. If you do not identify the risk, there is no way to control (avoid or reduce) or transfer the risk to insurance or contracts. Below, we will define the risks shared kitchens face, as well as insurance coverages and techniques that can be used to help protect against losses or reduce your risk.

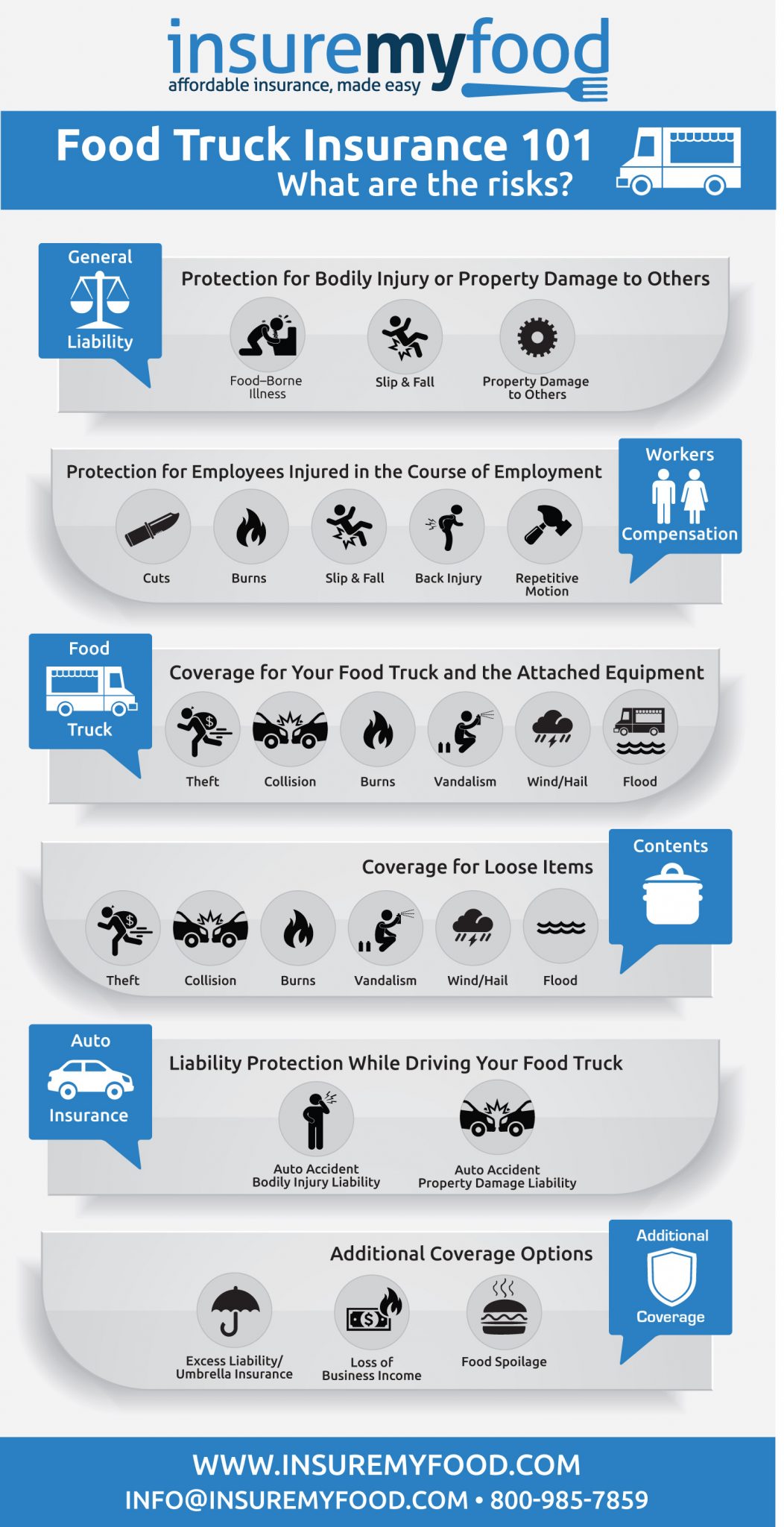

Liability Risk

As a shared kitchen, you are a landlord to many tenants working in a cooking environment. As with any landlord business, you owe a duty of care to offer a safe environment for your tenants. Accidents can happen for bodily injury or property damage to others, which is a risk inherent to running a shared kitchen. General liability insurance can help protect you from these accidents by providing coverage for accidents you are responsible for.

General liability is designed to protect you if your customer or public sues you for bodily injury or property damage. The coverage will pay your legal fees to defend, in addition to any awarded damages up to your policy limits. It’s important to note that “to others” means it does not cover your employees for injury, nor does it cover your own injury; those coverages fall under Workers Comp. In addition, property damage is also “to others”; it will not protect your own property from damage; this will fall under the property coverage discussed in that section.

Every shared kitchen should have general liability with limits of at least 1M per occurrence (per claim) and 2M aggregate (total per year for all claims), and your lease often requires this if you are renting your kitchen space. The lease will also often require you list the landlord as an Additional Insured (discussed in more detail later)

Tenants – General Liability

Now that you understand your responsibility for having general liability, you need to consider what risk your renters bring to you by being associated with them and providing the facility for their business.

If a renter causes an accident on your property, or the food they cook on your property causes injury to others, your kitchen most often will be named in the suit. An attorney, by default, is going to sue all involved parties regardless of the percentage of fault. Your general liability can protect you, but two issues arise. First, if the tenant does not have insurance, you will become the sole focus for liability, and two, these claims end up on your policy, causing your insurance to go up or be canceled.

The solution, and typically a requirement from your general liability insurance company, is that every tenant has general liability insurance and lists you as an additional insured on their policy. By being an additional insured*, you are protected alongside the tenant on their policy if they drag you into a claim from their actions. The result is you have transferred some of the risk your tenant brings to you by being protected by the tenant’s general liability policy.

*An additional insured is a standard policy endorsement with your kitchen’s legal name and mailing address listed. At your tenant’s request, their insurance agent will provide a certificate of insurance form called an Acord certificate of liability, also known as an Acord 25. This form will show the coverage limits, effective dates of coverage, and your kitchen as an Additional Insured.

*Important Note*

Most Additional Insured endorsements are on a blanket form. The blanket form means that a third party, such as your kitchen, is automatically an additional insured when required by a written contract or agreement. For the coverage to be valid, regardless of receiving a certificate, you need to have in your agreement with the insured that it is required to list you as an Additional Insured.

—

Tenant Damages

Shared kitchens often ask, what about my tenant damaging my kitchen property? There is limited coverage here for a fire the tenant causes and is negligent for, up to the sublimit for damage to rented premises, usually 100K-300K on most policies. However, the general liability is not designed to cover rented buildings for a broad range of losses. These losses are protected under property coverages, designed for property you own, or in your care, custody, or control.

At first glance, they may come as a shock, and be thinking, what if my tenant damages my expensive mixer or other equipment? Can’t I hold them liable? The answer is maybe, but it’s not going to be covered by their general liability insurance. This type of risk is why landlords often take deposits to offset some of this risk. There are solutions on property coverage, such as equipment breakdown, but this becomes an issue on the property policy because insurance was not designed to cover many different, ever-changing tenants in a building. With a one-off tenant, there are risk transfer solutions. With a shared kitchen it is not practical, nor realistic to have every tenant cover all the equipment in your kitchen on a property policy. This is for two reasons. One, can you really determine the tenant that solely caused the issue? More often, it is over time and several different tenants that lead to equipment failure. Two, the expense to have yourself, and every single tenant insure the same property would be cost prohibitive. All is not lost, though, as we will cover solutions for shared kitchens under the property section.

Property Risk

With your shared kitchen, you most likely invested a lot into your building, building improvements, and/or property and equipment.

To identify and classify different types of property coverages insurance covers, it is best to review how insurance companies define different types of property.

- Building – building coverage is designed to cover buildings you own at a specific address. If you lease your building, typically, the landlord will insure the building and pass the cost onto you via NNN in your lease. Note, just because you are reimbursing your landlord for their insurance cost to insure the building, you have no insurable interest in that policy, and it will not protect your business.

- Tenant Improvements – these are improvements you make to a leased building and things you cannot take with you at the end of the lease as they become the property of the landlord per most leases. These items include building walls, plumbing, and any built-in equipment.

- Business personal property – this is the contents you put in the space, such as equipment, tables, fridges, etc. These items typically are removed at the end of a lease.

NOTE: Pay careful attention to your lease. If there is existing property that you did not purchase but the landlord requires you to insure, for example, HVAC or existing walk-in cooler you will need to specify coverage for these items on your policy. Tenant improvements typically do not cover these items because you did not purchase or pay for these items, and they are by default part of building coverage. If you lease a building you do not have building coverage, causing a gap in coverage. However, that has not stopped landlords from transferring the risk of the equipment to their tenants.

What Does Property Insurance Cover

The types of losses that building, tenant improvements, and business personal property are covered below. Note, there are different types of coverage forms, and few areas of optional property coverages that some policies will leave off.

The broadest form is called Special Form, which covers all physical damage unless excluded. This means the burden of proof for a loss to not be covered is on the insurance company to prove its excluded. Common exclusions are food spoilage, earthquakes, floods, equipment breakdowns, power failures, neglect, intentional acts, and war.

The two other forms are Basic and Broad, which have list of coverages, and if its not in the list, there is no coverage. This puts the burden on the insured to prove there is wording to have coverage. It is best to avoid these forms unless no insurance company will offer you special form.

Theft Exclusions – Even with special form pay careful attention to exclusions added, the most common being a theft exclusion due to the nature of being a shared space, this increases the risk of theft, and some insurance companies will add a theft exclusion to make the risk acceptable.

Equipment Breakdown – this is a key coverage that all shared kitchens should seek coverage for and is not included without a specific endorsement. Equipment Breakdown pays for electrical or mechanical failure of equipment, such as walk-in coolers or other mechanical equipment.

Business Income – Business income is designed to pay your loss of profit and continuing expenses after you suffer a property loss. Often overlooked, this coverage is vital for a business to recover after a loss so you can stay afloat as your property is repaired and you can open back up for business. Typically, you will see this coverage listed a “Actual Loss Sustained – 12 months”, or specific limit with coinsurance (see coinsurance definition further below). There is a time element deductible that applies to these losses, typically 24 -72 hours after a loss, and then the coverage kicks in. This works like a deductible, but a time period must pass instead of a dollar amount for the coverage to start.

Replacement Cost vs. Actual Cash Value – Depending on how your property policy is set up, the insurance company will pay out claims differently, and the difference can be large. You either have a replacement value of the damaged property or equipment, which reimburses you for replacing the damaged property with new equipment. Or actual cash value, where depreciation is taken into account before paying the claim. For example, if you have a kitchen fire and your hood and grill are damaged, with replacement cost, the insurance company will pay for brand new equipment to replace the equipment. With actual cash value, if the hood and grill are ten years old at the time of the fire, the insurance company would only be required to pay the depreciated value of the equipment based on age and condition. Because it’s unlikely or difficult to replace old equipment with used equipment, this means you are likely paying the difference for deprecation for new equipment plus your deductible to get back up and running.

Coinsurance – Coinsurance is an often overlooked nuance in property insurance, and is not the same as coinsurance that you would see on medical insurance. The coinsurance limit on the policy is typically displayed right next to the limits of coverage and states the required insured-to-value limit. The most common coinsurance limit is 80%, but can vary from 70, 80, 90 or waived (not required), and is best explained by providing an example.

For example, if your requirement is 80% coinsurance, and you have 100K in business personal property but only insure it for 50K. You are insuring 50% of the value of the business personal property. Because you are below the 80% or higher requirement, the insurance company is only obligated to pay you 50% of your claim.

If you insured 80K or higher, in this same example, you met the requirement, and your claim would not be penalized. Keep in mind that in a total loss, they are still only going to pay up to the limit insured.

Admitted vs. Surplus insurance – There are two markets in the insurance world, and knowing the difference is essential. An admitted company is a company whose forms and rates are approved by the state. In addition, if the insurance company goes insolvent, the state will backstop the insurance company.

A surplus insurer is a market designed to take risks that do not have admitted insurance companies willing to offer coverage. With shared kitchens in many parts of the country surplus lines companies are the only ones willing to insure commercial kitchens because of the higher risk they face. These insurers are not regulated and can have customized coverage forms, exclusions, and higher costs. The key here is there is no uniformity. The easiest way to tell if you have a surplus policy is to see if taxes are charged on your premium.

Property of Others – Tenants Supplies, Inventory, and Food – Your property coverage does not cover your tenant’s property, and each tenant is responsible for insuring their own property, including spoilage. To avoid any confusion, it’s best to make this clear in a lease agreement with the tenant.

Situations can arise where you or another tenant unintentionally cause damage to another kitchen tenant’s property. In those cases, your general liability could be paid if you are directly liable for the damage. For example, you unplug a customer’s fridge by accident. If a pipe bursts in the kitchen or a power surge takes out a fridge, these would be examples where typically no liability occurs, and the tenant would need to claim on their own property policy.

Workers Compensation Risk

If your kitchen has employees, Workers Comp is an important coverage to protect against employee injuries, and in many states, the coverage is mandatory. This specific type of policy and coverage differs from general liability because general liability does not cover injured employees.

Workers Comp can pay for injury or disability to your employees injured on the job by providing medical, wage, and financial benefits per your state’s requirements. In addition, most policies come with employer liability coverage, which helps protect the business if you are sued for being negligent in the injury.

Note, paying an employee as a 1099 independent contract will not relieve your duty to be responsible for a workplace injury if they fit the definition of an employee. The IRS lists a full list of qualifications, but from a high level, if you tell them the hours to work, give them the tools for the job, or tell them how to do the job, they are legally employees.

Tenants Workers Comp – If your tenant has employees in your kitchen, it is a good idea to make sure the tenant has Workers Comp for their business. This helps prevent injuries that occur on your premises, blaming you if an employee is injured working but left with no recourse other than to try and hold your kitchen liable.

If you want to learn more about how Insure My Food can assist with your kitchen insurance, please complete our line form here.

Joel Paprocki, CIC, CRM, CPCU is founder of Insure My Food. Joel has over 20 years of experience in the insurance industry. He is passionate about helping food entrepreneurs navigate insurance and risk management with confidence. He holds all three top industry designations: Certified Insurance Counselor, Certified Risk Manager, and Chartered Property and Casualty Underwriter. He has served over 5,000 clients in the food industry, including restaurants, food truck, cateriers, If you are looking for a reliable, experienced, and specialized insurance partner, please contact us.

Joel Paprocki, CIC, CRM, CPCU is founder of Insure My Food. Joel has over 20 years of experience in the insurance industry. He is passionate about helping food entrepreneurs navigate insurance and risk management with confidence. He holds all three top industry designations: Certified Insurance Counselor, Certified Risk Manager, and Chartered Property and Casualty Underwriter. He has served over 5,000 clients in the food industry, including restaurants, food truck, cateriers, If you are looking for a reliable, experienced, and specialized insurance partner, please contact us.